Memory Chip Shortage Reshapes Global Smartphone Market: Samsung and Apple Thrive, Chinese Rivals Struggle Amidst Supply Crunch

A severe tightening in the global memory chip supply is dramatically reshaping the smartphone market landscape. This critical shortage is putting immense pressure on Chinese smartphone manufacturers while simultaneously boosting shipments for industry leaders like Samsung Electronics and Apple.

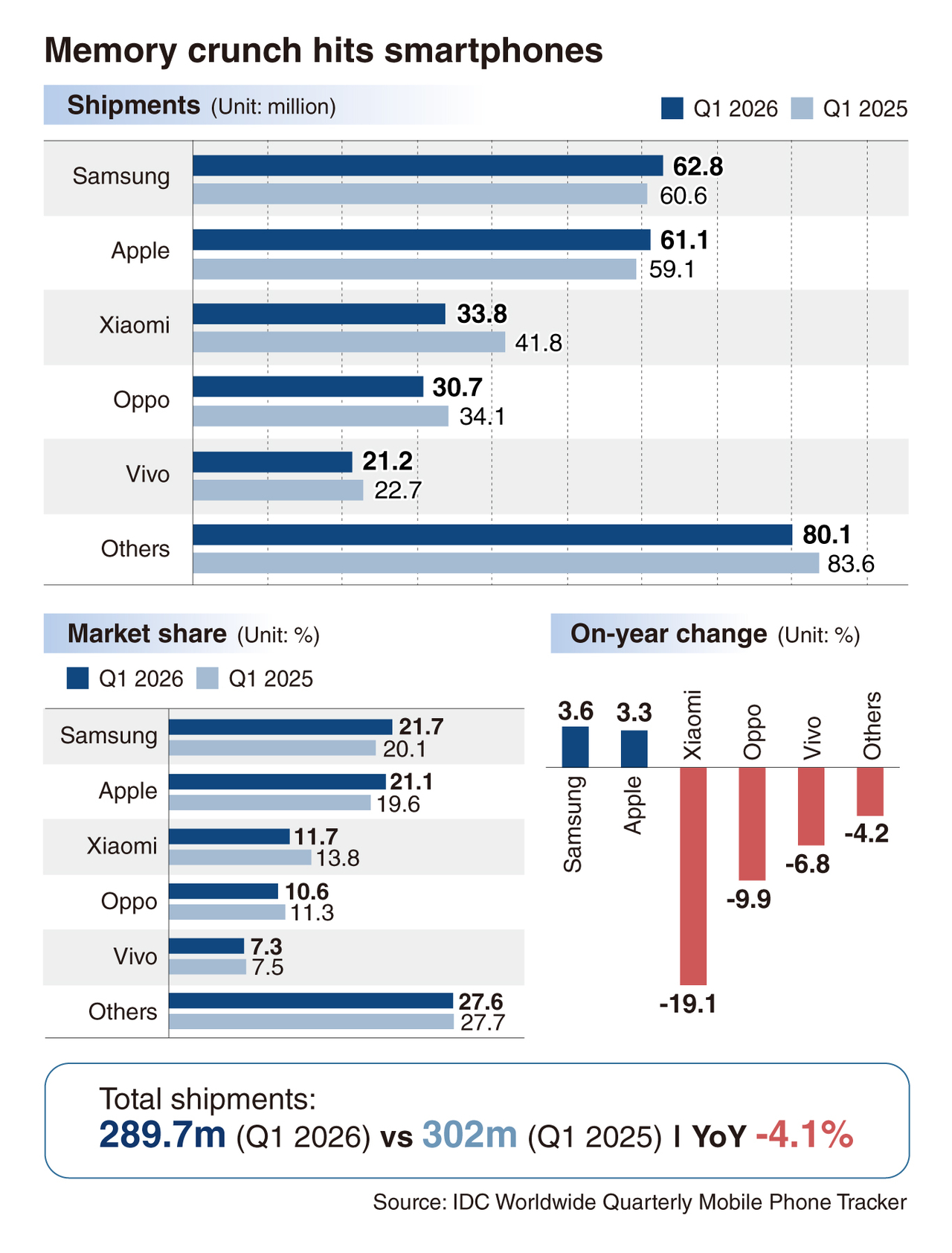

According to the latest report from market tracker International Data Corp. (IDC) on Tuesday, global smartphone shipments experienced a 4.1 percent year-on-year decline in the first quarter, reaching 289.7 million units. This marks the first such decline for the January-March period since 2023, signaling a significant shift in market dynamics.

Samsung claimed the top position with impressive shipments of 62.8 million smartphones, securing a 21.7 percent market share. Apple followed closely, shipping 61.1 million units and capturing a 19.6 percent share. Notably, Samsung and Apple were the sole brands among the top vendors to register year-on-year shipment growth, highlighting their resilience amidst the supply challenges.

In contrast, Chinese smartphone manufacturers experienced significant setbacks. Xiaomi dropped to third place with 33.8 million units, holding an 11.7 percent share, an 8 million unit decrease from the previous year. Oppo ranked fourth with 30.7 million units and a 10 percent share, while Vivo secured fifth place with 21.2 million units and a 7.5 percent share, all demonstrating a decline in market presence.

Industry experts attribute this divergence to a critical tightening in the supply of low-power DRAM (LPDDR), a vital component widely used in modern smartphones. Growing demand from Nvidia for LPDDR to power its next-generation graphics processing unit (GPU) platforms is severely straining the supply available for mobile devices. The U.S. chip giant is anticipated to incorporate substantial volumes of SOCAMM2, an LPDDR-based memory module crucial for AI servers, into its upcoming Vera Rubin GPU platform.

An anonymous industry source commented, “Apple possesses both the significant financial resources and strong bargaining power, enabling it to secure essential DRAM supply even at a premium. Samsung, leveraging its integrated structure, is also effectively minimizing procurement disruptions through seamless coordination between its mobile experience (MX) division and device solutions (DS) division.”

Market analysts predict that memory prices may only begin to stabilize in the latter half of 2027. Some warn that the LPDDR shortage could intensify further next year, particularly as Nvidia’s upcoming Vera Rubin Ultra platform is projected to demand even greater quantities of mobile DRAM, exacerbating current supply constraints.

For smartphone manufacturers, the ability to reliably secure memory chips is rapidly becoming as crucial as the process of designing and selling the devices themselves.

Samsung’s integrated business model provides a unique advantage, allowing it to coordinate effectively between its smartphone manufacturing and semiconductor operations, as the company operates extensive memory, system large-scale integration (LSI), and foundry businesses. While Apple does not possess its own memory unit, its 2025 10-K filing revealed a strategic reliance on long-term supply agreements and prepayment arrangements to guarantee the availability of critical components.

Recent high-profile meetings involving Qualcomm CEO Cristiano Amon with executives from Samsung and SK hynix are also being interpreted as part of broader, concerted efforts to secure crucial LPDDR supply for various industry players.

This challenging environment leaves Chinese smartphone vendors with limited options. Companies such as Xiaomi, Oppo, and Vivo lack both Samsung’s internal supply resilience and Apple’s formidable purchasing power, rendering them significantly more vulnerable to the ongoing LPDDR crunch and its consequences.

Their product portfolio further complicates the issue. Chinese vendors heavily rely on budget and midrange Android smartphones, segments where there is minimal flexibility to pass increased component costs onto price-sensitive consumers. IDC has indicated that rising memory prices are already pushing up smartphone average selling prices, with low-end Android vendors expected to bear the brunt of this impact.

Another industry source explained, “Chinese manufacturers have substantial exposure to budget and midrange models, making it exceedingly difficult for them to reflect higher component costs in their retail prices. If they raise prices, sales volume could plummet. If they maintain current prices, profitability will severely suffer. They are caught in a significant dilemma.”

IDC projects that the surge in memory prices and the persistent supply shortage will drive global smartphone shipments down by approximately 12.9 percent this year, reaching 1.12 billion units—the lowest level since 2013. This forecast underscores that the memory crunch is no longer merely a challenge for purchasing departments; it is fundamentally altering how smartphones are priced, manufactured, and distributed across the industry.

For Chinese vendors, the choices are indeed narrow. Passing on the escalating memory costs would inevitably erode their crucial price competitiveness, while absorbing these costs would further squeeze their already tight profit margins. Xiaomi’s smartphone gross profit margin stood at a modest 10.9 percent last year, making it particularly susceptible to even slight increases in core component costs.

“This unprecedented memory shortage has the potential to become a pivotal turning point, fundamentally reshaping the competitive hierarchy of the smartphone market,” stated an analyst at a local brokerage. “In the past, design innovation, camera capabilities, and price competitiveness were the primary differentiating factors. Moving forward, the proven ability to reliably secure essential core components will increasingly dictate shipments and ultimately, market share.”

yeeun