CXMT IPO Fuels Supply Surge: How Rising DRAM Risks Impact Samsung, SK Hynix, and Micron’s Pricing Power

ChangXin Memory Technologies (CXMT), China’s largest DRAM manufacturer, is accelerating its plans for an initial public offering (IPO) on Shanghai’s Star Market. The company aims to raise approximately 29.5 billion yuan ($4.3 billion) to significantly fund its capacity expansion efforts within the global memory market.

This anticipated listing, which industry sources suggest could occur as early as June, is intensifying scrutiny on the overall supply outlook in the global memory sector. The injection of new production capacity from CXMT could coincide with the current memory upcycle beginning to mature, potentially reshaping market dynamics.

CXMT is expected to strategically deploy the IPO proceeds to construct additional semiconductor production lines, bolstering its manufacturing capabilities.

CXMT IPO: Reshaping Global Memory Supply Dynamics

The move by ChangXin Memory Technologies is drawing considerable attention across the entire memory industry. CXMT has already disrupted the market by aggressively ramping up shipments of commodity DRAM, such as DDR4. This strategy often involves competitive pricing, exerting pressure on the industry’s established “big three”: Samsung Electronics, SK hynix, and Micron Technology.

This time, both the sheer scale of the IPO and its timing are particularly noteworthy. With substantial fresh capital poised to accelerate its expansion, CXMT could significantly boost its output precisely as global supply-demand dynamics begin to shift. This raises the distinct risk of the DRAM market becoming more balanced, or even experiencing an oversupply scenario.

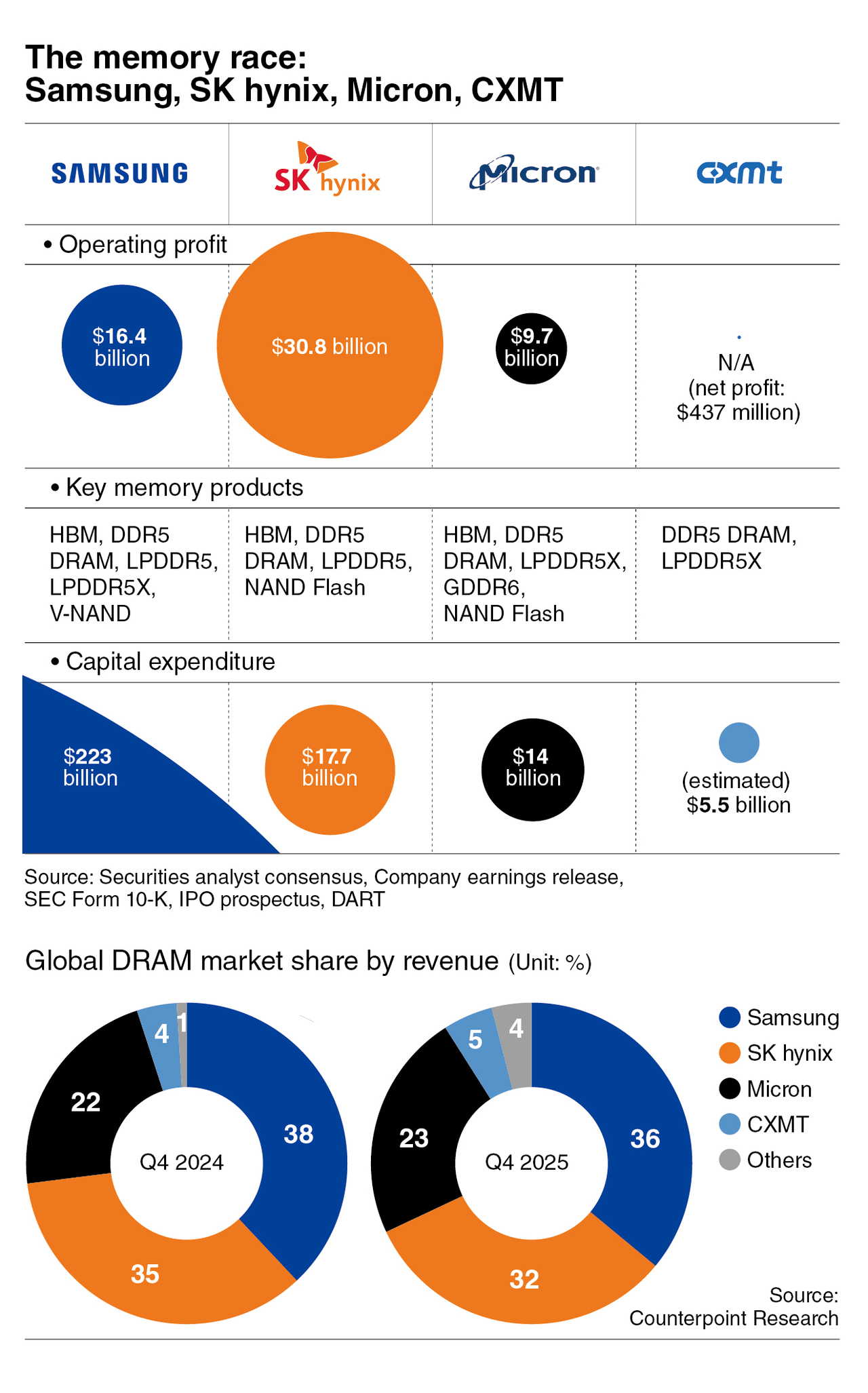

CXMT’s presence in the global DRAM market has expanded rapidly. As of the end of the third quarter last year, its market share reached 5 percent, marking a 2 percentage point increase from the previous year. Concurrently, its utilization rates climbed to an impressive 94.6 percent. This growth is mirrored by China’s NAND maker, Yangtze Memory Technologies, underscoring a broader strategic push by Chinese memory suppliers to gain market share.

DRAM Market Shift: From Scarcity to Potential Oversupply

The projected increase in CXMT’s DRAM output is now a significant factor influencing market expectations.

The tight supply conditions that primarily fueled the recent memory upcycle are anticipated to begin easing. This shift could reduce the urgency for front-loaded purchases by buyers. While a sharp price collapse is not considered the base scenario, market analysts predict a slower pace of price increases. Such a change would directly impact earnings momentum for key players in the memory sector.

This shift is particularly critical because the current market cycle has been largely driven by strong pricing power.

Samsung Electronics and SK hynix have reported robust earnings, particularly propelled by demand for high-bandwidth memory (HBM). However, commodity DRAM products still constitute a substantial portion of their revenue. If anticipated price gains fall short, their overall earnings growth is likely to decelerate.

Samsung, benefiting from the most diversified product portfolio, is actively expanding its high-value offerings, including HBM and advanced server DRAM. Nevertheless, segments like mobile LPDDR and PC DRAM remain significant revenue contributors. Its substantial exposure to Chinese smartphone and PC manufacturers could also leave it susceptible to increased pricing pressure as CXMT expands its domestic influence.

A slower increase in average selling prices (ASPs) would cap profit growth within Samsung’s memory business, especially given that current market forecasts often assume a strong pricing uptrend.

SK hynix faces similar market dynamics. While HBM has been its primary earnings driver, other segments, such as DDR5, remain highly sensitive to market pricing. This leaves its profitability exposed if the overall memory cycle begins to soften.

An industry source commented, “HBM is undoubtedly driving earnings right now, but commodity DRAM still forms the backbone of revenue. While high-value products are experiencing rapid growth, they are not yet sufficient to fundamentally alter the overall revenue structure. If commodity prices weaken, earnings growth will inevitably slow.”

The source further elaborated that price-sensitive segments, including server DDR5 and mobile memory, tend to reflect market shifts and impact profitability quite rapidly.

Long-Term Impact: CXMT’s Expansion and the Future of Memory Market Structure

Beyond the immediate implications for near-term supply, a more profound question revolves around how CXMT will strategically deploy its IPO proceeds.

It is improbable that the substantial funds will be allocated solely for commodity DRAM expansion. As China intensifies its pursuit of greater memory self-sufficiency, investment could potentially extend into higher-value, more advanced segments, such as HBM.

This scenario is where longer-term structural risks begin to emerge for the global memory industry.

Should CXMT successfully develop competitive HBM capabilities, the established market structure, currently dominated by three major players, could evolve into a four-player landscape. This would directly challenge the long-standing dominance of Samsung Electronics, SK hynix, and Micron.

For the immediate future, however, the direct impact is generally expected to be limited.

Lee Jong-hwan, a professor of system semiconductor engineering at Sangmyung University, suggested that the near-term effect on industry giants like Samsung and SK hynix would likely remain modest.

“Samsung is already investing on a much larger scale,” he stated, adding that while CXMT’s $4.3 billion fundraising is significant, it may not be enough to fundamentally reshape the global memory market landscape in the short term.

Nevertheless, this development is widely regarded as an early signal of a shifting competitive landscape within the semiconductor memory industry. It represents a scenario that could ultimately test the resilience of the current market structure as new production capacity and emerging players increasingly come to the fore.

yeeun