OLED Capacity Surge in China Threatens Price Wars, But Technology Remains Key Differentiator

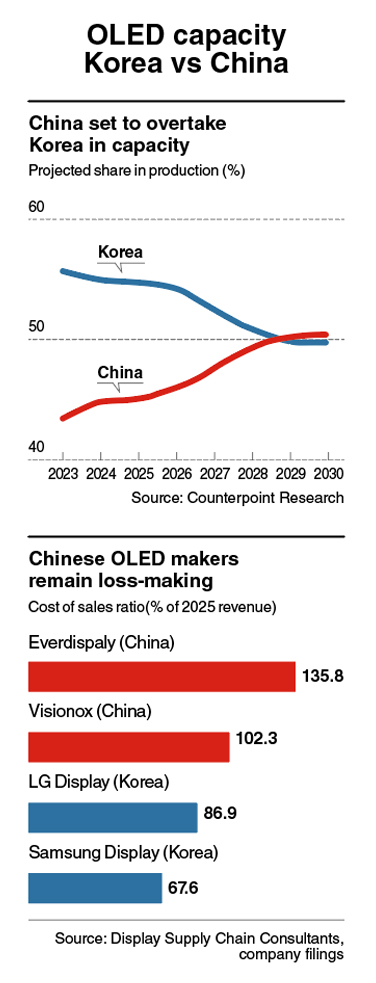

China is projected to surpass South Korea in OLED production capacity by 2029, fueling concerns that the industry may transition towards price-based competition, a trend similar to the LCD market’s evolution.

According to industry analysis from Counterpoint Research, Chinese panel manufacturers are rapidly investing in advanced production lines, including 8.7-generation fabs, closing the capacity gap with their Korean counterparts faster than anticipated.

Lee Jae-ho, a senior analyst at Counterpoint Research, suggests that Korea’s conservative expansion strategy could present a long-term structural disadvantage.

“While Korea maintains a strong OLED presence in mobile, IT, and TV sectors, investment in capacity expansion remains less aggressive compared to China,” Lee stated. “As seen in the LCD market, if China continues its rapid scaling, technological superiority alone may not be sufficient to maintain market leadership.”

Capacity vs. Competitiveness in the OLED Market

This forecast has reignited discussions about whether sheer production volume can equate to genuine competitiveness within the OLED sector.

Historically, in the display industry, scale has been a significant factor in determining pricing power. Increased supply typically leads to lower panel prices, often reshaping market share dynamics – a key element in China’s dominance in LCD technology.

However, industry experts emphasize that the OLED market operates under different principles.

“Capacity expansion alone doesn’t guarantee OLED competitiveness,” noted an industry source, who wished to remain anonymous. “The crucial factor is whether manufacturers can deliver the technology and performance levels demanded by global clients.”

Unlike LCD, OLED competitiveness heavily relies on yield rates, process stability, and the ability to meet stringent customer specifications.

“China may surpass Korea in capacity, but Korea currently leads in OLED technology,” stated Song Jang-kun, a professor of electronic and electrical engineering at Sungkyunkwan University.

China’s ascendancy in the LCD market resulted not only from scale, but also from a structural shift following a plateau in technological advancements.

As performance improvements became less noticeable to consumers, product differentiation diminished, shifting competition towards pricing, which favored manufacturers with larger production capacities.

Supported by substantial government funding, Chinese companies expanded aggressively, driving down prices and rapidly gaining market share, while Korean firms, operating on profit-driven models, struggled to keep pace.

This shift became apparent in the mid-to-late 2010s, as BOE and TCL CSOT increased investments in Gen 8.5 and larger fabs, reshaping the market around cost-driven competitiveness.

This experience fuels concerns that the OLED market could follow a similar trajectory. However, industry experts suggest such comparisons may be premature.

“LCD became vulnerable when technological differentiation narrowed, but OLED has not yet reached that stage,” explained Park Jae-geun, a distinguished professor at Hanyang University’s Department of Semiconductor Engineering.

With emerging applications like foldable devices, automotive displays, and AR/VR panels, technological demands continue to rise, keeping competition centered on innovation rather than price.

The disparity between Korea and China is also evident in profitability.

In 2025, Samsung Display reported a cost-of-sales ratio of 67.6 percent, while LG Display improved its ratio to 86.9 percent. Conversely, Chinese firms like Visionox and Everdisplay reported ratios of 102.3 percent and 135.8 percent, respectively, indicating losses on each unit sold.

Industry observers attribute this to fundamental differences in business models.

“Chinese OLED manufacturers have expanded capacity and market share through government support, but profitability remains weak due to low pricing and high fixed costs,” commented an anonymous industry source. “In many instances, investments are effectively sustained by subsidies rather than organic earnings.”

As competition intensifies, industry stakeholders increasingly emphasize that technology, not production volume, will determine long-term market leadership.

“Even with increased capacity, the critical question is whether companies are investing in technologies that meet actual customer needs,” another industry source noted. “Design flexibility and power efficiency have become crucial factors.”

The importance of low power consumption is amplified in the age of artificial intelligence, where energy efficiency is a key specification for IT devices.

Diverging OLED Investment Strategies

These contrasting priorities are reflected in companies’ investment strategies.

Chinese firms, backed by state funding, can continue capital expenditures even while operating at a loss, enabling rapid capacity expansion.

Industry estimates suggest that a single OLED fab investment in China can reach several trillion won (billions of dollars), with local governments often covering a substantial portion of the costs.

Korean companies, conversely, must rely on profits to fund investments, leading them to prioritize yield improvements, process optimization, and low-power technologies.

This results in two distinct approaches: China expanding capacity to gain market share, and Korea developing technology to maintain competitiveness.

Korea’s Edge in OLED Technology Remains

Global clients, especially US tech giant Apple, demand stringent standards in power efficiency, design flexibility, and reliability, mitigating the impact of capacity expansion alone.

Park added that these technological advantages are likely to persist in high-end segments such as automotive displays, laptops, and AR devices.

As OLED applications diversify, technological maturity and process capabilities increasingly shape the competitive landscape.

Currently, OLED remains firmly in a technology-driven phase, unlike LCD at its peak commoditization.

Whether this balance shifts will depend on how China’s capacity expansion reshapes supply dynamics, and whether Korean firms can maintain their lead in process innovation and customer-driven technologies.

yeeun