In the first quarter of 2026, **Samsung Display** and **LG Display** significantly expanded their foothold in the global **smartphone OLED panel market**. This impressive growth occurred even as the overall industry faced a notable contraction, primarily due to a surge in memory chip prices. This price hike compelled smartphone manufacturers to reduce production, with **Chinese competitors** disproportionately absorbing more than twice the volume decline compared to their Korean counterparts.

The **global smartphone OLED panel market** experienced a significant downturn in **Q1 2026**. Total **smartphone OLED panel shipments** decreased by 12 percent year-on-year, settling at 190 million units. This also represented a 20 percent drop from the previous quarter, as reported by Seoul-based market researcher **UBI Research** on Tuesday. While the post-holiday off-season contributed to the contraction, **UBI Research** identified production cuts by smartphone brands grappling with escalating **DRAM and NAND prices** as the dominant factor exerting pressure on **Chinese panel suppliers**.

Analyzing performance by origin, the combined **shipments** from **Samsung Display** and **LG Display** experienced a modest decline of approximately 7 percent year-on-year. In stark contrast, the four largest **Chinese suppliers** collectively reported a significantly steeper decrease of about 17 percent, highlighting the divergent impacts of market conditions.

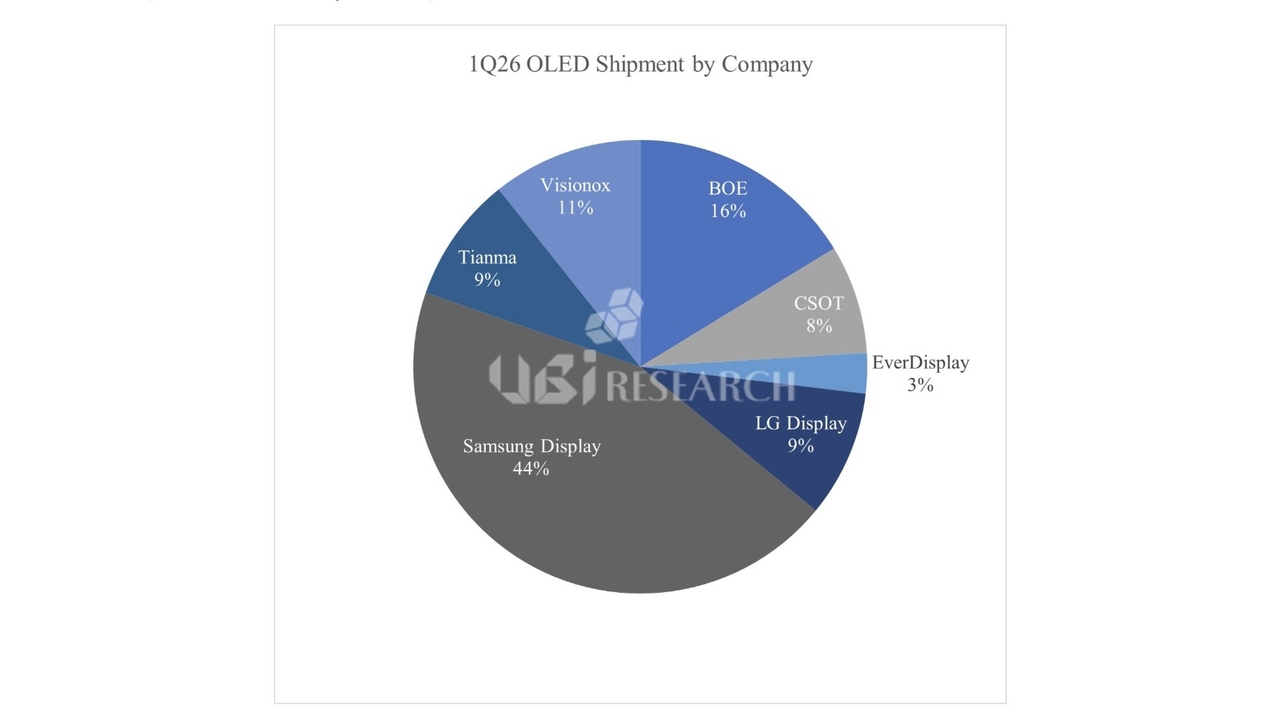

Despite the overall market downturn, **Samsung Display** solidified its position as the undisputed market leader. It commanded a formidable 44.4 percent **share** in the **smartphone OLED panel market**, an increase from 42.8 percent a year earlier. **LG Display** also demonstrated strong growth, expanding its share to 9.0 percent, up from 7.6 percent. Both Korean giants successfully gained **market share** even amidst a reduction in their absolute shipment volumes.

The performance among individual **Chinese panel makers** presented a mixed landscape. **BOE** maintained its lead as the largest Chinese supplier with a 16.3 percent market share. **Visionox** showed positive momentum, increasing its share to 10.7 percent from 9.3 percent. However, other prominent players faced headwinds: **Tianma** saw its share slide to 9.0 percent from 12.1 percent, and **TCL CSOT** experienced a drop to 7.8 percent from 9.8 percent.

**UBI Research** further elaborated on the trend, stating, “The impact of production adjustments by **Chinese smartphone brands** amid rising **memory prices** is being reflected primarily among **Chinese panel makers**.”

Looking ahead, **LG Display’s** full-year prospects remain robust, largely bolstered by its strong relationship with **Apple**. **UBI Research** projects an increase in the company’s **iPhone panel shipments** compared to the previous year. Industry analysts anticipate an additional lift, particularly with the eagerly awaited launch of the **iPhone 18 series** in the second half of the year.

mjh